Home » Archives for June 2012 » Page 2

Watching a baby take those first steps is exciting and a little nerve-wracking. Many parents wonder when it should happen and if their child is on track. Babies do not all walk at the same time, and that is normal. Some start early, while others take their time and focus on other skills first. I […]

Family bonding does not have to mean big trips or perfect plans. Most families just want simple ways to spend

Mental Health Awareness Month is a great time to pause, reflect, and talk openly about mental well-being. But many people

Many parents hear the term pediatric occupational therapy but are not sure what it really means or how it helps.

Managing money can feel overwhelming, but the right book can make it simple. Personal finance books break down topics like

Building a new home is exciting, but figuring out how to pay for it can feel confusing. You might be

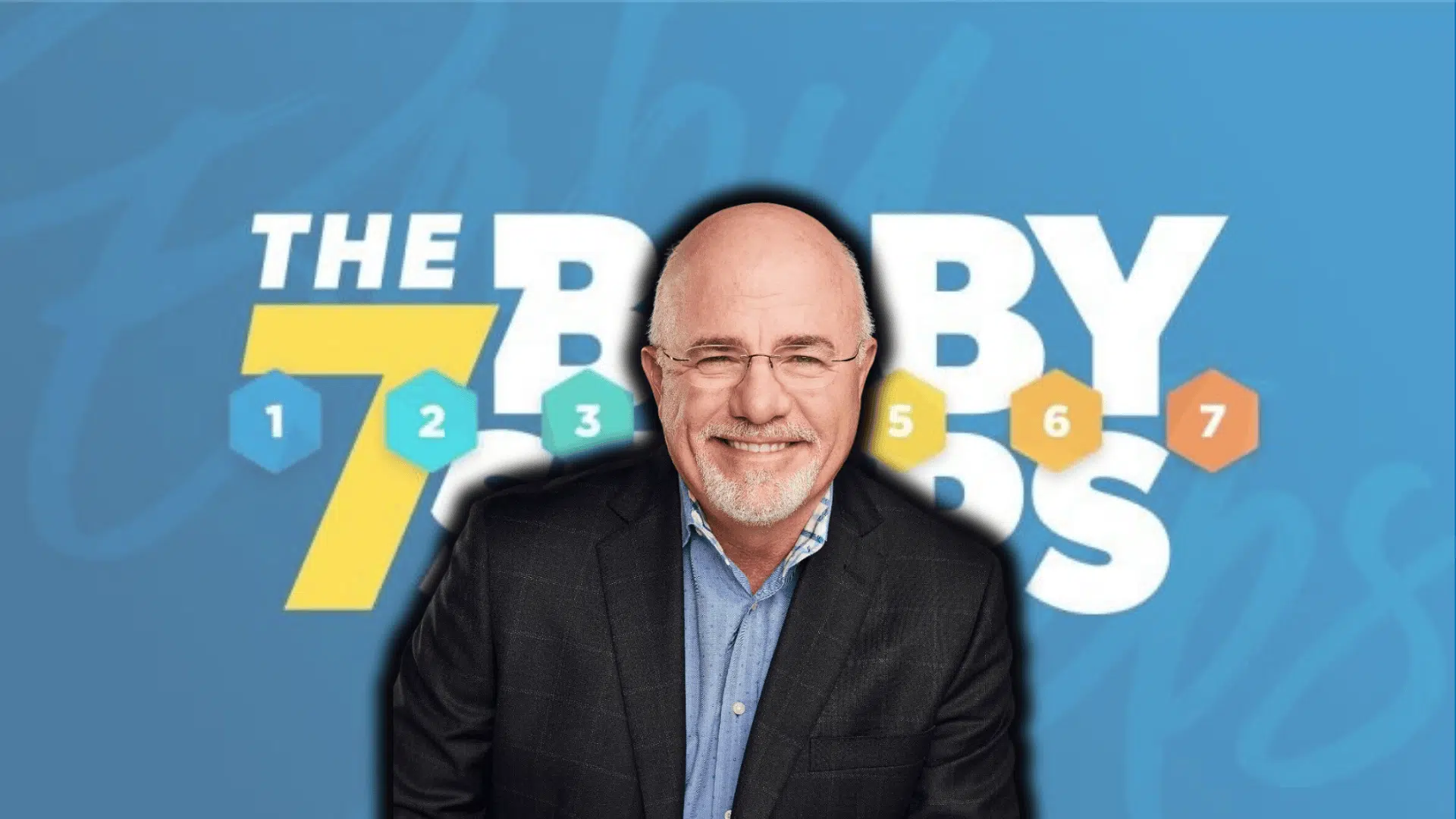

Managing money can feel overwhelming, especially when you’re juggling bills, debt, and future goals all at once. That’s where Dave